A Predictive CRE Property Price Index: the Holy Grail of Indices

CREtech Blog

I've been getting a little heat from folks at CoStar and others after my "Has Reaction Web Been Forgotten" post:

While most in the CRE biz enjoy a little CoStar bashing every now and then, that was not my intent. Instead, it was to suggest that there is a HUGE opportunity for CoStar to collect even more, very valuable data, in an efficient manner through their 2003 patent and the expertise of Reaction Web's team.

Allow me to explain.

By definition, every sale comp is historical. In other words, comps are lagging indicators and forever will be.

Currently, one of the only resources I am aware of which holds some level of predictive ability of future real estate capital market conditions is the PwC Real Estate Investor Survey. Because of how they survey market participants, they are able to capture market sentiment in a way a sale comp never will.

In economics, this is similar to the University of Michigan's Consumer Confidence Index survey, upon which Wall Street so heavily relies.

The Holy Grail for any index is to be leading indicator. If someone could build a commercial property price index which predicted commercial property price movement, they could charge a fortune, right?

You say, Impossible! I say, It is actually very possible.

In 2010, on Marketwi.se (a once killer, now defunct CRE blog) John Reeder wrote a post titled Technical Indicators and Cap Rate Spreads which used the trailing four quarter moving average of the spread between Cap Rates and the 10-year T-Bill as a technical indicator.

While Reeder acknowledged he had no empirical evidence to support whether a metric like this one would prove to be a useful leading indicator in the long run, it still felt like it would:

The interesting thing about the ideas that I am putting forward is that they really don’t have enough empirical testing to be relied upon. I don’t have the data that would be needed to go further back in time to test any thoughts I might have. But the reason that I throw these ideas out there is that I believe that something like this should work.

I would have to agree with him. At the same time, I think there is an even better way to predict commercial price movement.

Allow me to explain.

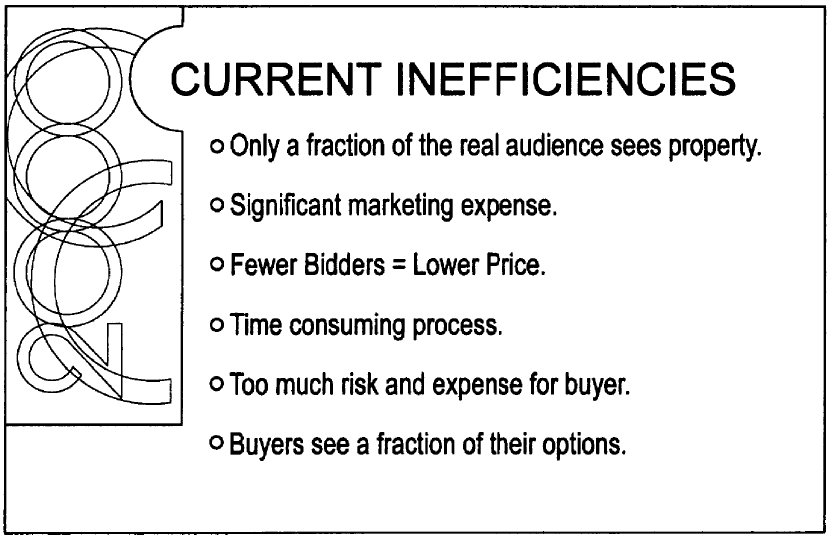

Within their 2002 patent, CoStar noted: Fewer Bidders = Lower Price.

{kind=link}

Or, alternatively, to points they make in future slides: More Bidders = Higher Price.

So, what if someone could monitor the number of bidders for each property and aggregate that data by asset type, asset class and region? This is similar to how CoStar segments their Commercial Repeat Sales Index already.

Tracking the number of bids on each deal would be pretty difficult, mainly because (i) a large number of bids are not submitted through an automated system (ii) brokers hate reporting anything to CoStar directly.

So, what is something which is easily tracked? How about signed confidentiality agreements?

After several years in the business, with one glance, many investment sales brokers can guess how many executed confidentiality agreements ("CAs") any potential listing would generate with great accuracy. This means the number of CAs are relatively predictable and usually dependent upon what property type is in vogue.

If you've ever been an investment sales broker, you'll know, the number of CAs signed has a strong direct correlation with the number of bids received.

By tracking the number of CAs executed on every deal, with the a decent algorithm, one could (even more effectively than experienced brokers) predict how many offers that listing could expect to receive.

A large majority of all CAs are now signed electronically, so tracking this data point would be relatively easy to do.

Sure, knowing the number of CAs signed or bids won't tell us what the property is going to ultimately sell for. But, remember, that's not the goal here.

The goal is to build a leading indicator to better predict movements in commercial property prices. In other words, will property prices rise or fall over the next 60 days?

By tracking the number of CAs executed on deals currently in the market, one could readily predict trends in market demand.

The closest thing to this type of Demand, Supply, Price index that I am aware of is the MIT/CRE TBI Index.

(Note where Demand fell in Q4 2006, and Supply and Price fell shortly thereafter.)

But even the TBI is not a real-time index. The time it takes to gather and report the information still makes the index a lagging indicator.

Recording the number of CAs executed and comparing it to a prior time period, one could theoretically predict trends in investor demand in real-time. Next to RCM, Reaction Web could quite possibly have access to the most CAs-signed data points outside of large national brokerage houses like CBRE or JLL.

So, if CoStar is truly interested in pursuing a data-centric business model, as I suggested in my prior post, then maintaining and building upon the platform Reaction Web created in the early 2000s could actually be very profitable.

Right now, CoStar's top two competitors for verified sale comp information are Real Capital Analytics and REIS. Neither of which have direct access to marketing or listing platform.

The reason I posed the question of whether Reaction Web was going to be forgotten was not to criticize CoStar's business practices, but instead, suggest there remains a HUGE opportunity to parlay Reaction Web's platform into a data gathering machine and obtain the Holy Grail: creating an index which could serve as a leading indicator for commercial real estate prices.

A note: we've considered creating an index like this using data from CREConsole.com's listings, but just don't have wide enough geographical coverage to generate reliable nation results.

--

Updated December 18, 2012 with clearer patent drawing exhibits.